To a first degree of approximation, transaction prices are the result of a balance between supply and demand for gas. This proposal is not expected to have an effect on the average supply of gas per block, nor on the demand for gas, nor on the marginal utility users extract out of transactions, so it’s not going to change the bottom-line transaction prices close to equilibrium.

It could conceivably lead to quicker convergence to equilibrium in some scenarios, but it could also lead to temporary oscillations as I’ve argued before, or fully prevent convergence (see [2102.10567] Dynamical Analysis of the EIP-1559 Ethereum Fee Market for a wonderfully detailed analysis that even reaches the conclusion that the base fee can show chaotic behavior in certain scenarios).

Will that lead to an overall improvement in the usability of the network as promised by the proposal? In order to answer that question one would first need to define what is meant by “usability” in a quantifiable language, which developers have been reluctant to do in this thread so far. Until then the promised benefits of this proposal are fully unfalsifiable. Is it worth taking a reduction in the cost an adversary needs to overcome in order to attack the network (which can be estimated readily) for such an uncertain benefit? (Or worse, prematurely switching the network consensus mechanism for such an uncertain benefit) I’d say no, until we have some quantitative understanding of what the benefit from this proposal is going to be.

I haven’t seen any evidence to suggest that the magnitude of underpayment is exactly equal to the magnitude of overpayment.

And if the network becomes more usable, then presumably demand would increase, and along with it the gas price. So we may never be able to isolate the one specific variable of overpayment caused by imperfect information and the resulting inefficiency.

Is chaotic behavior bad? And is the first-price auction not an exemplar of chaos?

Not sure what you are referring to with underpayment and overpayment, would you mind elaborating?

Yes, it would be fairly challenging to evaluate the effect of a change like this in production with a constantly changing environment, that’s why I’ve been advocating for quantitatively testing the assumption that this proposal is going to improve usability in a setting where it could be falsified. Many of the methods people have been applying in the simulation notebooks and various quantitative analyses would be adequate, but unless the outcome of an experiment has the ability to invalidate our thesis (which requires a precise enough definition of what we’re trying to achieve) we aren’t doing any science, we’re just using scientific language in order to give our opinion an aura of legitimacy.

Chaos is neither a bad nor a good thing in itself, it just imposes some barriers to our understanding. Even without bringing chaos into the picture it is easy to see that the base fee admits oscillatory solutions that might delay or prevent convergence to the equilibrium price (see the article I linked above if you’re interested), achieving the opposite of what people intuitively think this proposal is going to achieve. Hence my opinion that it would be risky to judge this proposal based on our intuition alone of what it ought to do because it is what people want it to do.

A basic economic equilibrium analysis is sufficient to realize that it cannot have much of an effect on the equilibrium price (which is IMO the most pressing problem the Ethereum community is facing). Of course that doesn’t rule out this proposal having some sort of secondary benefit. But what exactly? Will it outweigh the almost certain security costs? Will it outperform any of the cheaper and less controversial alternatives? Its counter-intuitive behavior suggests that those are all questions beyond the reach of our intuition alone, only a quantitative analysis can provide the answers.

That has little to do with the security cost I was referring to: With this proposal the cost that an adversary needs to overcome in order to conduct a 51% attack to the network is roughly halved (assuming that the block reward is approximately half of the current mining revenue), potentially divided by a greater factor if the fork is accompanied by substantial fragmentation of the existing hashrate into both branches of the fork and into other networks.

You might argue that an attack is still unlikely (which might be a valid assumption or not depending on the share of hashrate that moves over to London) so the expected cost to the network is still low, however so is the expected benefit (at least in relative terms compared to the exorbitant market-clearing prices we’ll have to continue paying), which is why I think it’s fair to ask whether one will outweigh the other, which I don’t think is a question we can answer without some quantitative modeling.

I don’t think it’s the primary objective of this proposal to reduce inflation, at least officially (I don’t question that its deflationary effect is the primary reason why some people are in such a rush to move forward with this proposal despite the lack of consensus and of conclusive evidence that it’s going to do more good than harm). And frankly, I think that the greatest mistake being made here is that this proposal conflates a monetary policy change (reduce inflation at the cost of security while precluding fixed supply) with a fee structure change (which is all it would take to achieve the promised usability improvement, whatever it is), even though it’s not technically necessary to make both changes simultaneously (even Tim Roughgarden makes this suggestion in the article you linked above). Result is a level of polarization not seen in years that might break the community in two over a “usability” change. I’m starting to think that will be a fair outcome.

So you’re legitimately predicting that the hashrate will drop by 50% solely due to this change? Does that mean you think that tips will converge to zero under 1559? The hashrate follows the ether price far more than the status of the block reward mechanism. That’s a historical fact. The same applies to every bitcoin halvening.

I’m pretty sure the hashrate is well higher than it was when ETH had a marketcap of $800 million, so I’m not worried, and it has been just about the most profitable coin to mine for as long as I can remember. If ETH is still the most profitable, why would any competent miner leave?

Remember that the entire point of Serenity is that miners should make zero dollars and zero cents per annum on the network. We want to discourage mining and encourage staking. If things go south after London hits mainnet, then at least we will have the necessary motivation to execute the merge.

To the extent that 1559 decreases inflation, reduces mining profitability, and increases usability, it really is killing three birds with one stone. Which other proposals are superior?

No, the revenue of that hashrate is expected to drop by ~50%, which as equilibrium is reached with the rest of the hashrate marketplace will allow an adversary to purchase a 51% share of the network hashpower at roughly half of today’s price.

That being accompanied by a hashrate drop is certainly a possibility to keep in mind, but it’s not central to my point and substantially more difficult to make predictions for: It could conceivably drop by under 20% or by over 80%, depending on how effectively miners coordinate to oppose this proposal.

Reducing the mining revenue to zero is reasonable as long as miners are not providing any useful service to the network, but like it or not they are the ones securing the network today, so cutting their revenue has direct security implications.

I’m a fan of Ethereum 2 just like you seem to be, but I’m not a fan of a rushed deployment of PoS as reaction to such a scenario, IMHO it would further compromise the security of the network. It would make a sustained attack easier than on the PoW chain and not really close any vulnerability (see my previous reply #320 for more of the background).

Hope you agree that killing birds #1 and #2 is as much of a liability as it is an advantage to the network, and that there is lacking material evidence that bird #3 would be killed by this proposal, particularly when compared with any alternatives able to increase the supply of gas per block even by a small percent, considering that gas supply scarcity is at the root of the current exorbitant gas pricing and ensuing usability problem.

@MicahZoltu What I see now is that if >50% of miners collude to send MINFEE to 0 (>60% of mining power now is against EIP-1559), then with miner-voted block size they can increase the block size to desired level and degenerate to current gas price auction but with elastic miner-voted block size.

Assuming that 100% of hashpower is available for rent to the highest bidder (even if the bid is a fraction of a penny higher) on short notice is the wrong assumption. Miner revenue has never been higher, and even Ethereum Classic is practically unaffected after multiple 51% attacks.

Again, what evidence is there that tips will magically converge to zero?

Literally no one is talking about the network today. London doesn’t launch today. EIP-1559 has zero effect on security prior to London.

So you admit that PoW security is insanely high right now. All the more reason to continue the march towards zero revenue. The longer miners go without a revenue cut, the more entitled they will feel to their current position. This is human nature.

If you enjoy participating in first-price auctions for everything you purchase, then more power to you. The rest of the world has other things to do with their time.

We have that already, and it’s fully compatible with 1559.

Not necessarily, the outcome is dependent on the reaction of the mining market to this proposal, if there is a large enough exodus of hashpower due to the decreasing profitability and/or the network splits into an EIP-1559 and a non-EIP-1559 fork with the latter receiving the larger share of the hashpower it doesn’t seem inconceivable for the liquidity of the hashrate rental pools to exceed the hashpower of the EIP-1559 network.

There is no implication in my argument that tips will converge to zero.

It doesn’t launch today but the consensus algorithm at launch time is expected to be PoW just as it is today.

I didn’t say that, even though I don’t rule out it might be higher than needed.

I didn’t say that either. All in all it would be helpful for the discussion if you cut down on the strawman arguments.

Yes, which makes the question of whether EIP-1559 will have any meaningful long-term impact on the usability of the network all the more relevant.

Miner rewards are currently about half block reward and half fees, and you say that revenue will drop by half after 1559. The block reward isn’t going anywhere. So explain how revenue would drop by half without tips approaching zero? Are you talking about a per hardware basis because hashrate will double? Or in terms of fiat currency because the price of ether will be cut in half?

Or is it because under 1559, miners will no longer be able to frontrun everyone else’s transactions without paying at least the basefee? Maybe that’s why blocks are so full these days. The dark forest is asserting itself.

Looking at https://etherscan.io/chart/blockreward current transaction fee rewards tend to oscillate between 1 and 4 ETH per block assuming ~6500 blocks per day. Assuming a mining tip of ~1 nanoeth per gas as suggested by other people in this thread and 12.5Mgas per block, that gives a drop of mining revenue between 0.987 and 3.987 ETH per block, or between 33% and 66% of the current security revenue.

This does not account for gas price auction (GPA) rewards, which will be largely unchanged. Those really high paying blocks tend to be rewards from GPAs.

You’re welcome to refine my estimate if you have any data on the magnitude and frequency of GPAs. Either way with that back-of-the-envelope confidence interval of ~33% it’s likely to fall within the same ballpark.

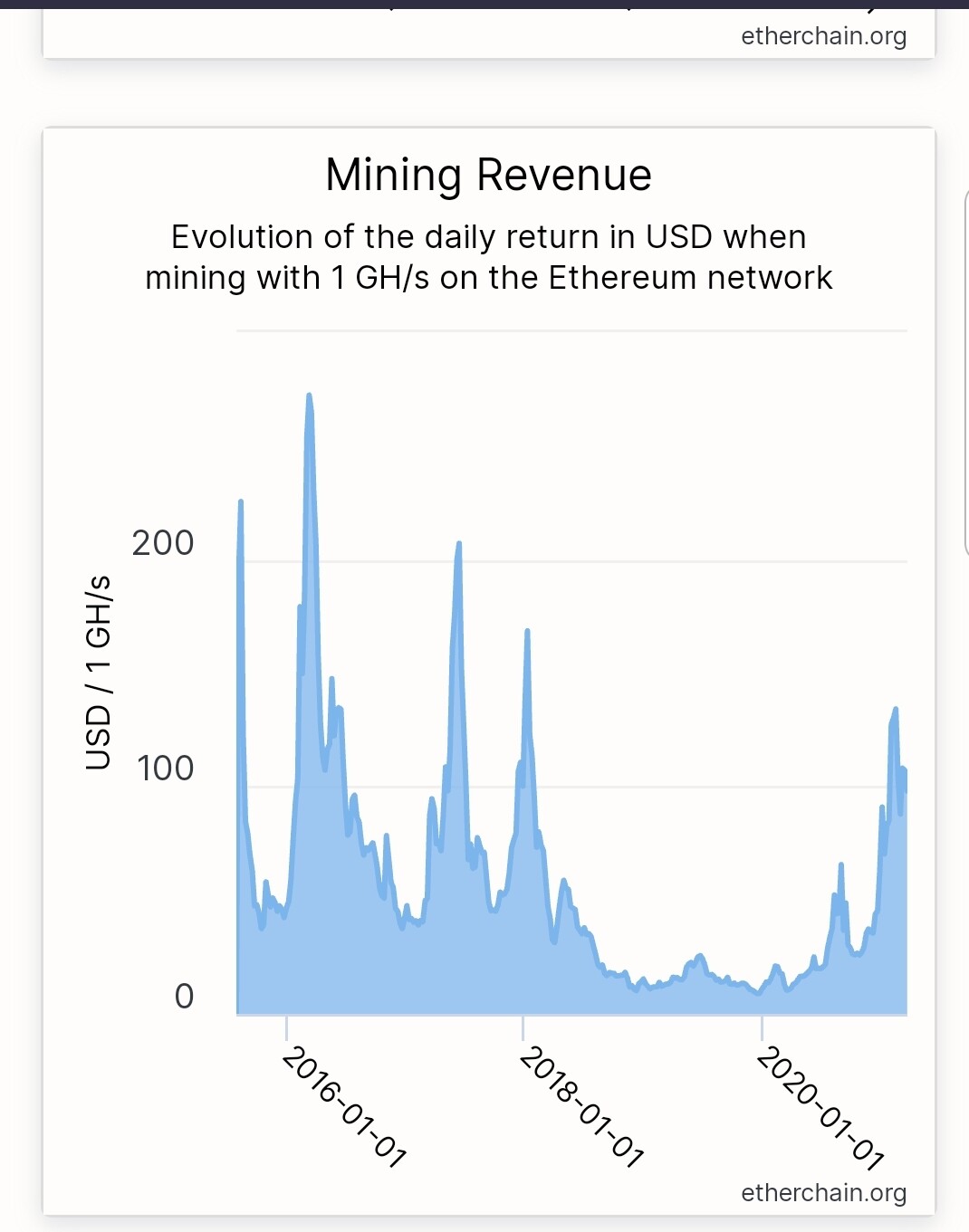

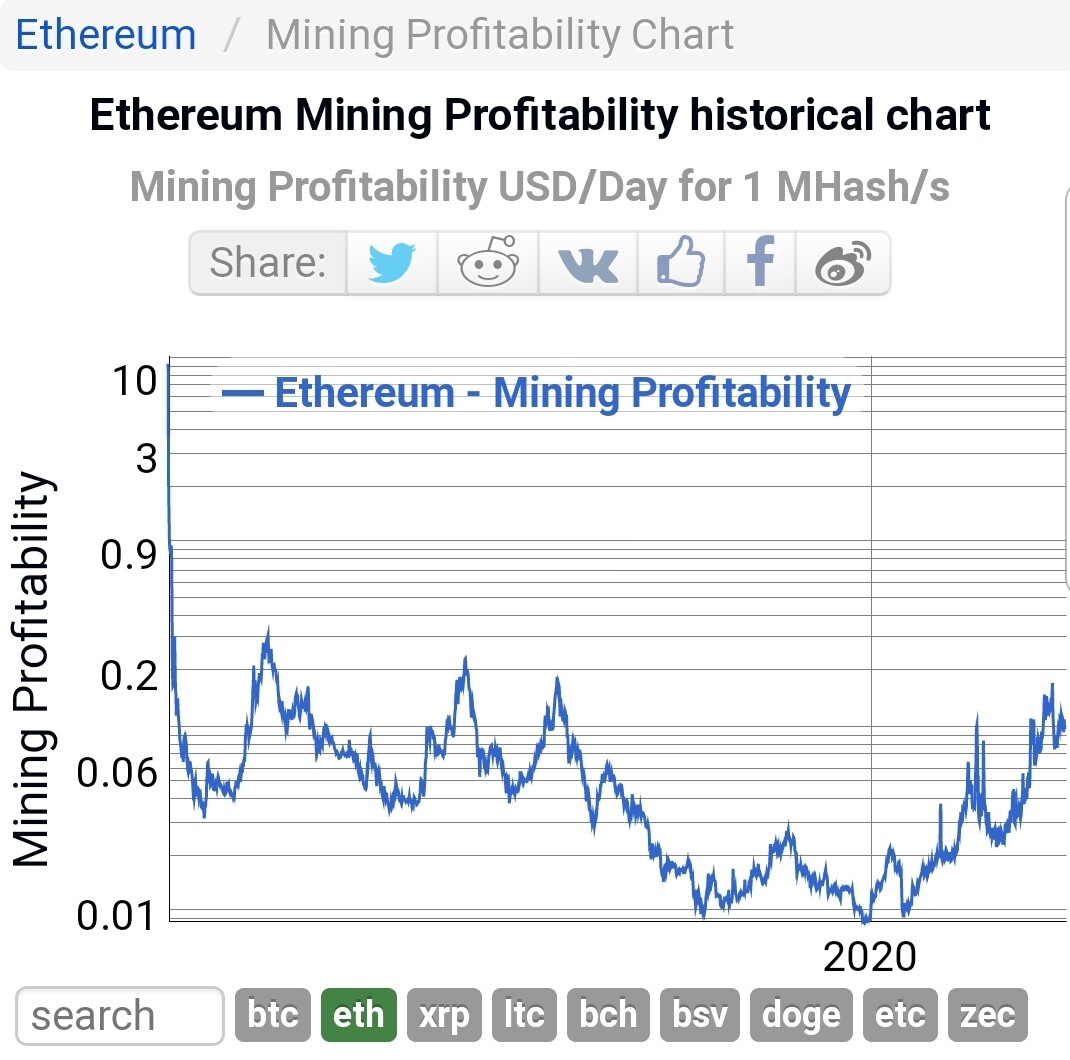

That’s per gigahash per second and per megahash per second. You’re looking at the wrong chart, lol. Which brings me to also say that a megahash has never been cheaper.

Median and average are not likely to fall within the same ballpark. The median tip is utterly irrelevant to the average. This is a classic mathematical blunder.

Nobody was talking about the median tip, I simply gave you some approximate lower and upper bounds justifying our expectation that this proposal is roughly going to halve the mining revenue,as you requested. Once again your constant use of straw man arguments (not to say needlessly insulting language) isn’t particularly helpful for this discussion, it doesn’t give the impression that you’re right, it only makes it look like you don’t have any better arguments to bring to this discussion other than misrepresenting other people’s points and then insulting them.

For a thorough simulation, see

For a thorough simulation, see